You made the right call. Bought early, held through the dip, watched it recover. Now your crypto is worth more than your car — and you can’t pay your electricity bill with it.

The utility company isn’t cruel. They just don’t speak your language yet. That tension, between real wealth and real life, is why finding the best crypto to fiat conversion methods matters more than most people admit.

This guide covers every way to cross it.

What Is Crypto to Fiat Conversion?

Crypto to fiat conversion is the process of exchanging a cryptocurrency, such as Bitcoin, Ethereum, USDT, or USDC, for a government-issued currency such as pounds, dollars, naira, or euros.

According to Bleap Finance, there are two ways this conversion happens. In explicit conversion, you actively sell your crypto and receive fiat. In implicit conversion, the crypto is converted automatically at the moment you pay or transfer, without you placing a separate trade.

The right method depends on three things: how fast you need the money, how much you are converting, and whether you need physical cash, a bank transfer, or just spending power.

Crypto-to-fiat exchanges are essential for crypto investors, allowing them to convert their digital assets into traditional currencies easily. This conversion enables individuals to use their funds fully without diving deep into the complexities of the crypto world.

Crypto to Fiat Conversion Methods

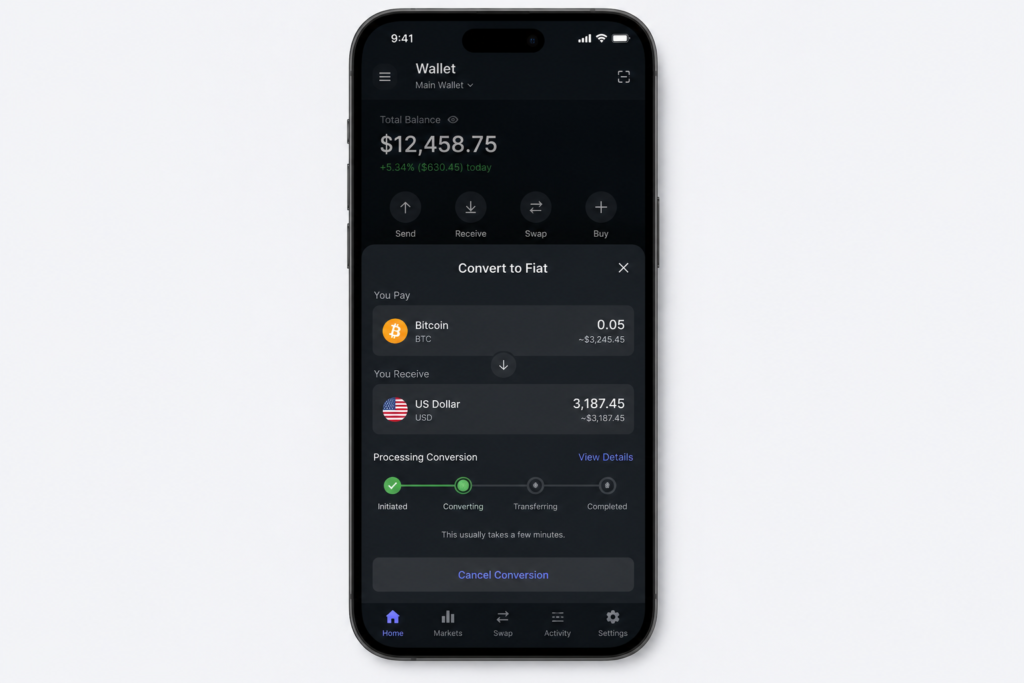

Method 1: Centralised Exchange (CEX)

A centralised exchange like Binance, Coinbase, or Kraken is the most widely used method for converting crypto to fiat.

The process is straightforward: you deposit your crypto into the exchange, sell it for your chosen fiat currency, and withdraw to your bank account via bank transfer.

Driven by advancements and new integrations like FedNow in the US and SEPA in Europe, some leading CEXs are drastically reducing fiat withdrawal times, offering settlement in minutes rather than days, though this speed depends heavily on the specific exchange and your bank.

Trading fees typically range from 0.1% to 1.5%, depending on your volume and the platform.

Best for: Large conversions, taking profit on investments, or anyone who wants funds in their bank account.

Watch out for: Withdrawal fees on top of trading fees, identity verification requirements (KYC), and processing times that vary by bank and region.

Method 2: Crypto Debit Card

A crypto debit card is a Visa or Mastercard linked directly to your crypto balance.

When you spend at a shop or online, the card converts the required amount of crypto to local fiat at the point of sale and processes a standard card transaction. The merchant receives fiat. You spend crypto.

This is what DEXTools describes as the fastest option for everyday spending: instant conversion at checkout, no separate step required.

Cards like the UPay card support BTC, ETH, USDT, and USDC at over 55 million Visa merchants worldwide with transparent cross-border fees of 1% to 2% in addition to any conversion spread embedded in the exchange rate.

Best for: Everyday spending, travel, international purchases, and anyone who does not want to withdraw to a bank first.

Watch out for: Conversion spreads embedded in the exchange rate, foreign transaction fees, and daily spending limits that vary by card tier.

Method 3: Peer-to-Peer (P2P) Trading

P2P trading platforms like Binance P2P and Paxful connect you directly with a buyer who wants to purchase your crypto. You agree on a price and payment method.

The platform holds your crypto in escrow until you confirm the buyer has paid.

Then the crypto is released to the buyer, and the payment arrives via your chosen method, which could be a bank transfer, mobile money, or even cash.

P2P offers several advantages. The fees are often the lowest available, ranging from 0% to 1%. You can choose buyers who pay via your preferred local payment method.

And the system works well for currencies and countries that mainstream exchanges do not always support well, including naira, cedi, and shilling conversions.

Best for: Users in markets with limited CEX coverage, those seeking flexible rates via negotiation, and anyone who wants to receive payment via mobile money or local bank transfer.

Watch out for: Slower than a card, requires trust in the buyer despite escrow, and dispute resolution can take time if something goes wrong.

Method 4: Off-Ramp APIs and Payment Processors

Off-ramp APIs like MoonPay, Transak, and Ramp Network are embedded directly into crypto wallets, DeFi apps, and Web3 platforms.

Instead of leaving your wallet to go to an exchange, you convert crypto to fiat without switching apps. The API handles the conversion, KYC, and settlement in the background.

According to Ramp Network, their solution supports Apple Pay, Google Pay, and card payments across 160 countries, with new payment methods added automatically.

Transak powers conversions for MetaMask users in 64 countries. These services typically charge between 1% and 3% but save significant time and friction for users who are already inside a Web3 application.

Best for: Users who want to convert crypto without leaving their wallet app, and developers building payment flows into Web3 products.

Watch out for: Fees can be higher than a direct CEX. Rates depend on the provider integrated into your specific wallet or app.

Read Also: How to Integrate Crypto Payments into a Website.

Method 5: Crypto ATMs

Crypto ATMs are physical machines that let you insert crypto and collect cash, or vice versa.

They require no bank account, no app, and in many locations no prior account setup. You walk up, select your currency, confirm the rate, send your crypto, and collect your notes.

The convenience comes at a price. Crypto ATM fees typically range from 5% to 15% of the transaction value, making them the most expensive method on this list.

They are best suited for situations where you need physical cash immediately and have no other option available.

Best for: Emergency cash needs, unbanked users, or situations where no other conversion method is accessible.

Watch out for: High fees, transaction limits, and not all machines support all cryptocurrencies. Always check the rate displayed on screen before confirming.

Choosing the Right Method for Your Situation

The right method depends on what you actually need:

- You need money in your bank account: Use a CEX. Sell your crypto, initiate a bank withdrawal, and wait. For large amounts, this is still the most reliable route.

- You want to spend at shops or online: A crypto debit card is the fastest and most convenient option. No bank involved, no separate conversion step.

- You want the best exchange rate: P2P trading allows you to negotiate rates, which can be favorable, though rates often include a premium over the spot market. Shop around among verified sellers before committing.

- You are inside a wallet or DeFi app: Use whatever off-ramp API the app provides. MoonPay and Transak are the most common.

- You need physical cash right now: A crypto ATM is your only option, but factor the fee into your decision.

Note: The following information is specific to the UK (HMRC) and may not apply to your country.

Tax on Crypto to Fiat Conversions

Important Disclaimer: Tax laws governing crypto are different in every country. Below is a key example, but you must consult a local tax professional for your jurisdiction.

In the UK, HMRC treats every crypto-to-fiat conversion as a taxable disposal. The gain or loss between what you paid for the crypto (cost basis) and what you received in fiat is either a capital gain or a capital loss.

If you receive crypto as income, such as from DeFi yield or freelance payments, that income is taxable at the point of receipt.

Keep records of every conversion: the date, the amount of crypto, the fiat value received, and the exchange used.

Crypto tax tools like Koinly, Cointracker, and TaxBit can automate most of this if you connect your exchange accounts.

If you are in any doubt about your obligations, speak to a tax professional who has experience with digital assets before the end of the tax year.

Read Also: How USDT payment works.

Conclusion

Converting crypto to fiat is not complicated once you understand the options.

CEXs are reliable for bank withdrawals. Crypto cards are the fastest for everyday spending.

P2P offers the best rates. Off-ramp APIs handle the conversion inside your existing wallet.

Crypto ATMs are the last resort, but require no bank.

The biggest mistake most beginners make is using the wrong method for the situation: paying ATM-level fees for a transaction that could have gone through a CEX for a fraction of the cost, or waiting three days for a bank transfer when a crypto card would have handled it instantly.

Know your options. Calculate the real cost. Choose accordingly.